Authors: Janine Barlsen, Jule Hüneke, Isabella Joneck, Svea Kuhlmann

Last updated: September 30th 2023

1 Definition & Delimitation of Concepts

Pressing social and environmental issues as well as the public discourse related to them increasingly require firms to make investments in corporate sustainability and corporate social responsibility. Yet at the same time, in a capitalist system, firms also face the pressure of generating profits, usually requiring them to build business cases for their activities. In general, a business case can be defined as “a pitch for investment in a project or initiative that promises to yield a suitable significant return to justify the expenditure”1 Carroll, A. & Shabana, K. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. International Journal of Management Reviews 12(1), 85–105 (2010). or shorter an “action or investment with a positive cost/benefit ratio”.2 Suchanek, A. & Lin-Hi, N. Business Case. https://wirtschaftslexikon.gabler.de/definition/business-case-123490/version-384766 (2021). Given that firms use business cases to justify investments, the question arises whether there is a business case for or of sustainability-related activities: Does it pay to be green or good? And if so, when and where? Answering these questions is important, since, if sustainability pays, this will make it much easier for managers and employees to argue why related investments are necessary or possible. Also, it is important to know which types of investments pay and which don’t, since it seems plausible that companies might primarily pursue those activities that pay and neglect those that do not. In this sense, understanding the business case for sustainability is not only of direct relevance for those firms that seek to implement sustainability but also to understand the progress of corporate sustainability more broadly.

1.1 Definition

There is no uniform definition of the “business case for sustainability.” However, in the literature some authors – especially Schaltegger et al. (2012, 2018, 2019) – distinguish between a “business case of sustainability” and a “business case for sustainability.“3Schaltegger, S. & Lüdeke-Freund, F. The „Business Case for Sustainability“ Concept: A Short Introduction. https://ssrn.com/abstract=2094238 (2012).,4Schaltegger, S. & Burritt, R. Business cases and corporate engagement with sustainability: Differentiating ethical motivations. Journal of Business Ethics 147, 241-259 (2018).,5Schaltegger, S., Hörisch, J. & Freeman, R. E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Organization & Environment 32(3), 191–212 (2019).In the following, the difference between the two terms as discussed in the literature shall be briefly presented. Given that the scientific literature focuses more on the business case for sustainability (BCS) and shows a somewhat heterogeneous picture regarding the definitions, in the following sections, the term “business case for sustainability” will be used as an umbrella term to describe research dealing with the question of “(when) does it pay to be green/good”.

The “business case of sustainability” builds on the assumption that the primary motive of firms is to make profits and that sustainability serves as a means to this greater end.6 Jones, K. P., King, E. B., Nelson, J., Geller, D. S., & Bowes-Sperry, L. (2013). Beyond the business case: An ethical perspective of diversity training. Human Resource Management 52, 55-74 (2013).7Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business cases for sustainability: The role of business model innovation for corporate sustainability. International Journal of Innovation and Sustainable Development 6, 95-119 (2012).It assumes that the three dimensions of sustainability (economic, environmental, social) are not equally important but that the economic dimension is most important. Instead, the starting point of this approach is economic success and not the intrinsic motivation to integrate sustainability and thus all three dimensions holistically into the company. Rather, the underlying notion is that environmental and social activities can serve as potential avenues for achieving favorable financial outcomes. This leads to the assumption that sustainability measures are only considered and implemented if they ensure economic success for the company, for example by reducing costs in production. Managing a business case of sustainability is seen as “the result of opportunistic behavior”.7Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business cases for sustainability: The role of business model innovation for corporate sustainability. International Journal of Innovation and Sustainable Development 6, 95-119 (2012). Moreover, by prioritizing profit maximization, this perspective construes business success narrowly as profit optimization, neglecting the broader concept of value creation.8Gray, R. Social, environmental and sustainability reporting and organisational value creation? Whose value? Whose creation? Accounting. Auditing & Accountability Journal 19, 793-819 (2006).

In contrast to the concept of the “business case of sustainability,” the “business case for sustainability” puts much greater weight on social and environmental dimensions, proposing that economic success can and should emerge through conscious and intelligent integration of environmental and/or social aspects.9 Perceva, C. Towards a process view of the business case for sustainable development: lessons from the experience at BP and Shell’. Journal of Corporate Citizenship 9, 117–132 (2003). , 4Schaltegger, S. & Burritt, R. Business cases and corporate engagement with sustainability: Differentiating ethical motivations. Journal of Business Ethics 147, 241-259 (2018)., 5Schaltegger, S., Hörisch, J. & Freeman, R. E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Organization & Environment 32(3), 191–212 (2019). The starting point of a business case for sustainability is not the generation of profit in the first place but rather the resolution of a social or ecological problem. The consideration of sustainability as a solution to the mentioned problem may lead to economic success. Therefore, the economic success is the result but not the primary purpose of the implementation of sustainability measures in a company.5Schaltegger, S., Hörisch, J. & Freeman, R. E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Organization & Environment 32(3), 191–212 (2019). 5Schaltegger, S., Hörisch, J. & Freeman, R. E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Organization & Environment 32(3), 191–212 (2019). Also, the literature suggests that companies that adopt the approach of a “business case for sustainability” instead of the “business case of sustainability” put less emphasis on trade-offs between the different dimensions of sustainability but try to create synergies between economic achievements and a comprehensive integration of sustainability within business frameworks. Also, an important difference between the “business case of sustainability” and the “business case for sustainability” is that in the latter case the improvement of sustainability performance is seamlessly integrated into the core mission of a company.7Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business cases for sustainability: The role of business model innovation for corporate sustainability. International Journal of Innovation and Sustainable Development 6, 95-119 (2012). Furthermore, this approach suggests that economic success can and should arise through strategic sustainability management.4Schaltegger, S. & Burritt, R. Business cases and corporate engagement with sustainability: Differentiating ethical motivations. Journal of Business Ethics 147, 241-259 (2018).,10Weber, M. The business case for corporate social responsibility: A company-level measurement approach for CSR. European Management Journal 26, 247-261 (2008). Schaltegger et al. (2019) summarize a business case for sustainability as “creating economic success through (and not just along with) a certain environmental or social activity”.5Schaltegger, S., Hörisch, J. & Freeman, R. E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Organization & Environment 32(3), 191–212 (2019).

Table 1 summarizes the most important difference between the “business case of sustainability” and the “business case for sustainability”.

| Business case of sustainability | Business case for sustainability | |

| Motivation | Economic success | Solution to ecological/social problem |

| Role of sustainability | Opportunity for creating profits | Contribution to sustainable development Part of solution to social/ecological problem |

| Trade-offs in sustainability dimensions | Focus on identifying trade-offs | Focus on creating/using synergies |

| Relationship business & sustainability performance | Dichotomous concepts | Dichotomous concepts, which need to be aligned to create triple win solutions |

1.2 Components of a business case for sustainability

Schaltegger et al. (2019) define three requirements that characterize business cases for sustainability and simultaneously state the difference between the hierarchic view of a business case of sustainability and the interconnected perspective of business cases for sustainability using synergies. The three requirements are the following:

- Voluntary corporate initiatives for solution of social and ecological problems

Rather than just complying with regulations or legal mandates, activities that build the basis of a business case should be voluntary and aim to improve society or the environment. Additionally, these actions and activities also must go beyond the conventional notion of business purpose to exclusively generate profit.

- Measurable positive economic outcome of the initiatives

For the evaluation as a business case, the initiatives and activities of the company must be able to generate a positive economic effect for the company. The holistic implementation of sustainability as goal and starting point of the business case for sustainability remains and thus implies the simultaneity of sustainability and economic success.

- Causal link between management actions and desired outcomes

A business case for sustainability requires a causal link between the corporate activities and their intended outcome of solving social or ecological problems and a positive economic effect.5Schaltegger, S., Hörisch, J. & Freeman, R. E. Business Cases for Sustainability: A Stakeholder Theory Perspective. Organization & Environment 32(3), 191–212 (2019).

1.3 Interrelationship Business Case for Sustainability and other concepts

Business Model Innovation

The scientific literature repeatedly shows a link between the BCS and business model innovation.7Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business cases for sustainability: The role of business model innovation for corporate sustainability. International Journal of Innovation and Sustainable Development 6, 95-119 (2012). That such a connection of both concepts exists and that this is also meaningful and important, becomes clear when comparing the definitions. As presented above, the business case for sustainability arises from the motivation to solve a social or ecological problem and to achieve a positive economic outcome for a company despite this or precisely because of this. Schaltegger et al. (2012) define business model innovation for sustainability as “supporting voluntary, or mainly voluntary, activities that solve or moderate social and/or environmental problems”.7Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business cases for sustainability: The role of business model innovation for corporate sustainability. International Journal of Innovation and Sustainable Development 6, 95-119 (2012). Thus, the definition of business case and business model innovation for sustainability imply the interrelationship of these two concepts. An integrated view of both concepts is therefore useful and necessary when analyzing and dealing with the BCS and the question, whether it pays to be green or good.

Creating Shared Value (CSV)

Furthermore, literature has depicted a link between the business case for sustainability and the theoretical framework of Creating Shared Value (CSV) as an “approach for articulating the business case for corporate sustainability”.11 De los Reyes, A. & Scholz, M. The limits of the business case for sustainability: Don’t count on ‘Creating Shared Value’ to extinguish corporate destruction, Journal of Cleaner Production 221, 785 -794 (2019). Porter and Kramer (2011) define CSV as “policies and practices that enhance the competitiveness of a company while simultaneously advancing social and economic conditions” implying a relationship to a business case for sustainability concept.12Porter, M. E. & Kramer, M. R. The big idea: Creating shared value. How to reinvent capitalism—and unleash a wave of innovation and growth. Harvard Business Review 89, 62–77 (2011). Nevertheless, literature shows a controversial view on the CSV concept, debating whether CSV is just a buzzword for existing concepts (e.g. business case for sustainability), an extension or a new, independent concept as analysed by Menghwar and Daood (2021).13Mengwhar, P. & Daood, A. Creating shared value: A systematic review, synthesis andintegrative perspective. International Journal of Management Reviews 23, 466-485 (2021).Therefore, the interrelation between the two concepts must continue to be researched.

2 Literature review

2.1 Origin of the Business Case for Sustainability

The business case for sustainability and the question “does it pay to be green or good” have their roots in a historical debate whether companies that live up to their socially and ecologically ascribed responsibility are economically more successful than others. Thus, a business case is expected to exist if a “firm does well by doing good”.14McWilliams, A., Siegel, D. & Wright, P. Corporate Social Responsibility: Strategic Implications. Journal of Management Studies 43 (1), 1-18 (2006). In the literature, the relationship between social and ecological responsibility and economic success has been investigated by investigating the links between the concepts of “Corporate Social Performance (CSP)/Corporate Ecological Performance (CEP)” and “Corporate Financial Performance (CFP)”.15 Schreck, P. Der Business Case for Corporate Social Responsibility. in Corporate Social Responsibility: Verantwortungsvolle Unternehmensführung in Theorie und Praxis (eds. Schneider, A. & Schmidpeter, R.) 71–88 (Springer Berlin Heidelberg 2015).,16Salzmann, O., Ionescu-Somers, A. & Steger, U. The Business case for corporate sustainability: literature review and research options. European Management Journal23(1), 27–36 (2005).,3Schaltegger, S. & Lüdeke-Freund, F. The „Business Case for Sustainability“ Concept: A Short Introduction. https://ssrn.com/abstract=2094238 (2012).

Literature on the subject must be divided into different analytical frameworks and models. The first research wave until 2000 used mainly qualitative measures to capture the environmental performance.17 Hoang, T., Przychodzen, W., Przychodzen, J. & Segbotangni, E. Does it pay to be green? A disaggregated analysis of U.S. firms with green patents. Business Strategy and the Environment29(3), 1331-1361 (2020). The literature in this time provides information about the CSP/CEP and CFP relation by using a linear model, with either positive, negative or neutral outcomes. 18Griffin, J. & Mahon, J. The corporate social performance and corporate financial performance debate. Business & Society 36, 5-31 (1997). Furthermore, it distinguishes between considering three causal effects resulting in different hypotheses and outcomes.19Hang, M. & Geyer-Klingeberg, J. It is merely a matter of time: A meta-analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment28(2), 257-273 (2019).:

- the influence of CSP/CEP on CFP,

- the influence of CFP on CSP/CEP

- a bidirectional relationship

While studying the causal effect of CSP/CEP on CFP seems most obvious, the reverse relationship (an effect of CFP on CSP/CEP) may appear not as intuitive. However, it is important to consider that environmental and social investments may not only contribute to financial success of firms but that the financial success of firms also enables companies to invest in sustainability, as it provides them with the necessary resources.

The first few debates on the link between CSR and business benefits already occurred in the 1950s.1Carroll, A. & Shabana, K. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. International Journal of Management Reviews 12(1), 85–105 (2010).The start of an intensive debate on the CSP/CEP and CFP link and thus the cornerstone of the development of the business case for sustainability can be traced back to Milton Friedman’s (1970) statement that “the social responsibility of business is to increase its profits” in the 1970s.20Friedman, M. The social responsibility of business is to increase its profits. New York Times SM (1970).,21Trumpp, C. & Guenther, T. Too little or too much? Exploring U-shaped Relationships between Corporate Environmental Performance and Corporate Financial Performance. Business Strategy and the Environment 26, 49-68 (2017).

Friedman´s statement fueled the debate about the relationship between CSP/CEP and CFP and the question “does it pay to be green”, resulting in heterogenous results which will be shown in the following.21Trumpp, C. & Guenther, T. Too little or too much? Exploring U-shaped Relationships between Corporate Environmental Performance and Corporate Financial Performance. Business Strategy and the Environment 26, 49-68 (2017).

Effect of CSP/CEP on CFP

Negative Relationship

The first hypothesis emerging in the field, was the trade-off hypothesis, which builds on the consideration of the impact of CEP/CSP on CFP. The hypothesis, based on Milton Friedman’s statement, suggests that the implementation of environmental aspects in operational decisions weakens the financial success of a company, because the costs of implementation exceed its economic benefits.22Preston, L. & O’Bannon, D. The corporate social–financial performance relationship. A typology and analysis. Business and Society 36(4), 419–429 (1997).The hypothesis was scientifically presented in the study by Bragdon, Jr. and Marlin (1972) analyzing results that a company is either economically successful or acts responsibly, but an agreement of both is impossible.23Bragdon, J., Jr. & Marlin, J. ls Pollution Profitable. Risk Management 19, 9–18 (1972). Furthermore, research by Vance (1975) and Aupperle et al. (1985) state a competitive advantage for companies, which do not invest in CEP/CSP, as they do not bear the costs of implementation and thus support the trade-off hypothesis.24Vance, S. Are socially responsible corporations good investment risks. Management Review 64(8), 19-24 (1975).,25Aupperle, K., Carroll, A. & Hatfield, J. An empirical examination of the relationship between corporate social responsibility and profitability. Academy of Management Journal 28(2), 446–463 (1985).

Positive Relationship

In the course of scientific investigations, new hypotheses emerged that contradict the trade-off hypothesis. One hypothesis is the so-called, social impact hypothesis which is based on Latané (1981).26Latané, B. The psychology of social impact. American Psychologist 36(4), 343–356 (1981). According to this hypothesis, companies should address implicit stakeholder expectations, including environmental responsibility. Studies of McGuire et al. (1988) show that failing to do so can heighten market risks and the likelihood of more stringent agreements, while environmentally conscious firms experience improved financial performance.26Latané, B. The psychology of social impact. American Psychologist 36(4), 343–356 (1981).,19Hang, M. & Geyer-Klingeberg, J. It is merely a matter of time: A meta-analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment28(2), 257-273 (2019).,27McGuire, J., Sundgren, A. & Schneeweis, T. Corporate social responsibility and firm financial performance. Academy of Management Journal 31(4), 854–872 (1988).

Later, a hypothesis that has received considerable attention in the scientific community is the win-win hypothesis or Porter hypothesis, which posits a positive impact of CEP/CSP on CFP. In their study, Porter and van der Linde (1995) refer to the economic benefits of a national environmental policy, refuting the trade-off between economics and ecology. Additionally, they argue that improved CEP through government regulations leads to implementation of environmental aspects. A more efficient use of resources in the long run for example, resulting in a competitive advantage for companies while lowering emissions. Thus, creating a win-win situation.28Porter, M. & van der Linde, C. Toward a new conception of the environment–competitiveness relationship. Journal of Economic Perspectives9(4), 97–118 (1995).

Another hypothesis put forward at a similar time is the natural resource-based view (NRBV) based on studies by Wernerfelt (1984), Barney (1991) and Hart (1995).29Wernerfelt, B. A resource‐based view of the firm. Strategic Management Journal5(2), 171-180 (1984).,30Barney, J. Firm resources and sustained competitive advantage. Journal of Management 17(1), 99–120 (1991).,31Hart, S. (1995). A natural-resource-based view of the firm. Academy of Management Review 20(4), 986–1014 (1995) According to this literature a firm’s strategy and competitive advantage receive considerable influence from its environmental performance. The central driving factors encompass pollution prevention, product stewardship, and sustainable development. Moreover, the studies strengthening the NRBV state that a firm’s strategic advantage can be derived from its ability to access strategically valuable resources within its individual resource bundle.31Hart, S. (1995). A natural-resource-based view of the firm. Academy of Management Review 20(4), 986–1014 (1995),29Wernerfelt, B. A resource‐based view of the firm. Strategic Management Journal5(2), 171-180 (1984).,30Barney, J. Firm resources and sustained competitive advantage. Journal of Management 17(1), 99–120 (1991). Furthermore, early analysis by Davis (1973) underpins the later developed NRBV, that corporate environmental stewardship leads to long-term profit maximization while doing good for society.32Davis, K. The case for and against business assumption of social responsibilities. Academy of Management Journal16(2), 312–322 (1973).

The instrumental stakeholder theory that emerged at the same time supports the NRBV presented earlier.33Donaldson, T. & Preston, L. The stakeholder theory of the corporation: Concepts, evidence, and implications. Academy of Management Review 20(1), 65–91 (1995).,34Jones, T. Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review 20(2), 404–437 (1995). Jones (1995) study highlights that environmental initiatives that go beyond a compliance level satisfy stakeholder expectations and are therefore characterized as a proactive eco-governance strategy. Such a strategy, according to research results leads to increased reputation through a transparent display of ecological stewardship, which translates into improved stock market performance.34Jones, T. Instrumental stakeholder theory: A synthesis of ethics and economics. Academy of Management Review 20(2), 404–437 (1995). Thus, the study suggests a positive relationship between CEP/CSP and CFP.

Effect of CFP on CSP/CEP

Negative relationship

A hypothesis that suggests a negative causal effect of CFP on CEP/CSP is the managerial opportunism hypothesis.35Weidenbaum, M. & Vogt, S. Takeovers and stockholders: Winners and losers. California Management Review29(4), 157–168 (1987).,22Preston, L. & O’Bannon, D. The corporate social–financial performance relationship. A typology and analysis. Business and Society 36(4), 419–429 (1997).,36Posner, B. & Schmidt, W. Values and the American manager: An update updated. California Management Review 34(3), 80–94 (1992).Literature by Weidenbaum and Vogt (1987) indicate that managers prioritize their personal goals over shareholder interests which can lead to operational inefficiencies, driven by short-term profit incentives and stock prices. Consequently, environmental investments may suffer, affecting CEP.35Weidenbaum, M. & Vogt, S. Takeovers and stockholders: Winners and losers. California Management Review29(4), 157–168 (1987).

Positive relationship

The slack resources theory developed in a similar period asserts a positive impact of CFP on CEP.37Bourgeois, L. On the measurement of organizational slack. Academy of Management Review 6(1), 29–39 (1981).,38Kraft, K. & Hage, J. Strategy, social responsibility and implementation. Journal of Business Ethics 9(1), 11–19 (1990).,22Preston, L. & O’Bannon, D. The corporate social–financial performance relationship. A typology and analysis. Business and Society 36(4), 419–429 (1997).Research by Kraft and Hage (1990) suggests that this is because favorable financial performance generates slack resources that companies can allocate to environmental initiatives.38Kraft, K. & Hage, J. Strategy, social responsibility and implementation. Journal of Business Ethics 9(1), 11–19 (1990). Similar to the NRBV hypothesis, investing in such activities enhances internal resources, capabilities, and competitiveness, allowing for innovation and eco-friendly developments as a study by Bourgeois (1981) shows.37Bourgeois, L. On the measurement of organizational slack. Academy of Management Review 6(1), 29–39 (1981). However, literature states that limited financial resources might hinder firms’ desire for environmental and social actions, potentially leading to short-term ecological investments when financial slack is available.22Preston, L. & O’Bannon, D. The corporate social–financial performance relationship. A typology and analysis. Business and Society 36(4), 419–429 (1997).

Neutral Relationship

The supply and demand framework was developed by McWilliams and Siegel (2001) and follows the premise that an optimal environmental investment, which integrates both shareholder interests and the needs of stakeholders such as customers, employees and communities can be achieved through a cost-benefit analysis. They conclude that the same principles should apply to environmental investment decisions as to any other investment. Companies that follow this model achieve comparable profitability, assuming they make optimal decisions and are in market equilibrium.39McWilliams, A. & Siegel, D. Corporate social responsibility: A theory of the firm perspective. Academy of Management Review 26(1), 117–127 (2001). The supply and demand theory can also be applied for a neutral relationship in the causal relation CEP/CSP on CFP.

Bidirectional Effect

Considering both previously presented causal effects together, is called virtuos circle according to Waddock and Graves (1997).40Waddock, S. & Graves, S. The corporate social performance-financial performance link. Strategic Management Journal 18(4), 303–319 (1997). It states that “CSP is both a predictor and consequence of financial performance”40Waddock, S. & Graves, S. The corporate social performance-financial performance link. Strategic Management Journal 18(4), 303–319 (1997). In their study, they confirmed the hypothesis that “better financial performance results in improved CSP” and “improved CSP results in better financial performance, ceterus paribus.” (Waddock and Graves 1997). Therefore, there might be a positive simultaneous and integrative impact, a virtuous circle as named by the authors.40Waddock, S. & Graves, S. The corporate social performance-financial performance link. Strategic Management Journal 18(4), 303–319 (1997). Nevertheless, the other depicted hypotheses also indicate a negative, as well as a neutral causality in both directions.

In summary, the historical roots of the relationship between CEP/CSP and CFP and the inferred (non-)existence of a business case for sustainability are built on a very heterogeneous basis. Early literature on this topic cannot clearly answer the question, “does it pay to be green” and thus state the existence of a business case for sustainability. Instead, as the historical literature review points out, various hypotheses and theories have been developed, confirming the heterogeneity of the findings. Later literature, as will be shown below, has further explored the heterogeneous data and expanded the question of the existence of a business case for sustainability.

2.2 Status quo: Current status of literature reviews

Given the importance of the business case for sustainability, it is not surprising that the relationship between CEP/CSP-CFP remains an important topic of current research. In fact, in the past decades empirical literature studying the relationship between CEP-CFP has grown rapidly. Similar to the historical research, studies have investigated the question of “does it pay to be green/good?”. In this context, controversies emerged regarding the sign of relation and the causality of the effect.41Feng, M., et al. Green supply chain management and financial performance: The mediating roles of operational and environmental performance. Business Strategy and the Environment: forthcoming, 27(7), 811-824 (2018).,42Hartmann, J., & Vachon, S. Linking environmental management to environmental performance: The interactive role of industry context. Business Strategy and the Environment, 27(3), 359–374 (2018).,43Hang, M., Geyer‐Klingeberg, J., & Rathgeber, A. W. It is merely a matter of time: A meta‐analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment, 28(2), 257-273 (2019). As a result, in addition to investigating the direct link between CEP/CSP and CFP, scholars have increasingly focused on studying moderating and mediating factors to better understand when and why it pay to be green or good?”.

Next to relevant primary studies, which mostly analyse the relationship via data collected from companies and databases, meta-analyses find wide application in the research of this subject matter. Meta analyses are a quantitative review method, which standardizes and aggregates findings across existing quantitative empirical studies. Given the vast number of studies that have been published on the CEP/CSP-CFP link with differing results, this method has been proven to be useful to understand and consolidate the state of research.44Damanpour, F. Organizational innovation: A meta-analysis of effects of determinants and moderators. Academy of Management Journal, 34, 555-590 (1991). In fact, a considerable number of meta studies have been published in recent years on the CEP/CSP-CFP link that provide a good overview of the field. Therefore, the following literature review section predominantly draws on findings published in meta analyses.

Literature review from 2000 until present

To tie in chronologically, the following part introduces empirical studies and their conclusions of the last two decades.

One study that had an important influence on the field was the one by Orlitzky, Schmidt & Rynes (2003) who conducted a meta-analysis to investigate the cause-and-effect-relationship of CSP and CFP.45Orlitzky, M., Schmidt, F. L., & Rynes, S. L. Corporate social and financial performance: A meta-analysis. Organization studies, 24(3), 403-441 (2003). They found a positive and significant correlation between the two, indicating that companies with better CSP also tend to exhibit better financial performance. The study also highlighted the importance of considering contextual factors and industry characteristics when assessing this relationship. The authors retrospectively refer to the hypotheses mentioned in Chapter 2.1 and state that the trade-off hypothesis is not supported by the results reflecting the last 30 years of research. Additionally, the authors emphasized the need for more rigorous research methods and standardized measures to further enhance the understanding of the link between corporate social responsibility and financial outcomes.45Orlitzky, M., Schmidt, F. L., & Rynes, S. L. Corporate social and financial performance: A meta-analysis. Organization studies, 24(3), 403-441 (2003). The demand for a uniform research method and standardised measures is also repeatedly expressed in ensuing studies.

Horváthová’s (2010) findings also support a positive CEP-CFP relation, implying that companies with stronger environmental performance tend to experience improved financial performance. While a positive correlation between environmental and financial performance is generally observed in the study of Horváthová, various factors such as industry dynamics, regulations, regional contexts, and methodological differences can contribute to occasional negative correlations observed in other studies.46Horváthová, E. Does environmental performance affect financial performance? A meta-analysis. Eco-logical economics, 70(1), 52-59 (2010). After two primary studies also revealed a negative CEP-CFP relation, namely Ameer and Othman (2012)47Ameer, R., & Othman, R. Sustainability practices and corporate financial performance: A study based on the top global corporations. Journal of Business Ethics, 108(1), 61–79 (2012). and Makni et al. (2009)48Makni, R., Francoeur, C., & Bellavance, F. Causality between corporate social performance and financial performance: Evidence from Canadian firms. Journal of Business Ethics, 89(3), 409–422 (2009)., Horváthová extended these results in 2012 and demonstrated that there is an intertemporal effect that has an impact on the relation. She states that CEP is leading to CFP decrease after one year, but that after several years the firms would profit from CEP. She thus confirms that her findings are consistent with the Porter hypothesis in the long run.49Horváthová, E. The impact of environmental performance on firm performance: Short‐term costs and long‐term benefits? Ecological Economics, 84, 91–97 (2012).

Another very influential, major meta-analysis is the one conducted by the authors Dixon-Fowler et al. (2013) that were able to reconfirm the results of Orlitzky et al. (2003) and therefore concluded that the BCS could be proven, thus summarising: “It does pay to be green”.50Dixon‐Fowler, H. R., Slater, D. J., Johnson, J. L., Ellstrand, A. E., & Romi, A. M. Beyond “does it pay to be green?” A meta‐analysis of moderators of the CEP–CFP relationship. Journal of Business Ethics, 112(2), 353–366 (2013).,45Orlitzky, M., Schmidt, F. L., & Rynes, S. L. Corporate social and financial performance: A meta-analysis. Organization studies, 24(3), 403-441 (2003).

Friede, Bassen & Busch (2015) motivate their study by pointing to a lack of a uniform methodology and inconsistencies in previous results on the CEP-CFP relationship. Their study is based on a greater number of primary and secondary studies, which is why more robust results can be obtained. They evaluate the relationship of Environmental, Social and Governance (ESG) and CFP and conclude that roughly 90% of studies find a nonnegative ESG-CFP relation. Additionally, they highlight, that there is a large majority of research with positive findings and that the positive impact of ESG on CFP appears stable over the period.51Friede, G., Busch, T., & Bassen, A. ESG and financial performance: aggregated evidence from more than 2000 empirical studies. Journal of sustainable finance & investment, 5(4), 210-233 (2015).

Endrikat, Guenther & Hoppe (2014) published another meta-analysis at the time, focusing on the direction of causality and the multidimensionality of the focal constructs. Their results indicate that a generally positive and partially bidirectional CEP-CFP relationship exists. Moreover, the results suggest that this relationship is more robust when CEP is strategically proactive rather than reactive. The study also uncovers moderating influences of methodological biases, which partly explain the inconsistent outcomes observed in previous research.52Endrikat, J., Guenther, E., & Hoppe, H. Making sense of conflicting empirical findings: A meta-analytic review of the relationship between corporate environmental and financial performance. European Management Journal, 32(5), 735-751 (2014).

Wang et al. (2016) focused on the causal relationship between CSR and CFP. They concluded that future financial performance is linked to preceding social responsibility efforts, whereas there is no evidence supporting the opposite direction. Therefore, these findings correspond to the instrumental stakeholder theory.53Wang, Q., Dou, J., & Jia, S. A meta-analytic review of corporate social responsibility and corporate financial performance: The moderating effect of contextual factors. Business & society, 55(8), 1083-1121 (2016).

In the context of studies concentrating primarily on the cause-and-effect relationship, the term “u-shaped relationship” is increasingly used in the more recently published studies. The study by Trumpp & Guenther (2017) examines this more precisely and explores the idea that extremely high or extremely low levels of environmental performance might lead to suboptimal financial outcomes.54Trumpp, C., & Guenther, T. Too little or too much? Exploring U‐shaped relationships between corporate environmental performance and corporate financial performance. Business Strategy and the Environment, 26(1), 49-68 (2017). The research finds support for the u-shaped relationship, indicating that both very poor and excessive environmental performance could potentially be associated with diminished financial performance. The authors are speaking of the ‘too-little-of-a-good-thing’ effect (TLGT), when companies with low CEP tend to have a negative link to CFP and companies with superior CEP tend to have a positive link. According to Trumpp and Guenther, TLGT integrates the trade-off hypothesis, managerial opportunism hypothesis, win–win hypothesis, resource-based view (RBV), NRBV and instrumental stakeholder theory within the context of corporate environmental performance and financial performance (CEP–CFP), which were mentioned in chapter 2.1. Additionally, the study underscores the importance of finding an optimal balance between environmental and financial goals. It suggests that moderate levels of environmental performance are generally associated with the best financial outcomes, aligning with the notion of a u-shaped relationship.54Trumpp, C., & Guenther, T. Too little or too much? Exploring U‐shaped relationships between corporate environmental performance and corporate financial performance. Business Strategy and the Environment, 26(1), 49-68 (2017). In brief, according to Trumpp & Guenther, whether the relationship between CEP and CFP is positive or negative depends on the level of CEP.

On the contrary, the study by Hang, Klingeberg & Rathgeber (2018) provides evidence confirming the Porter hypothesis and slack resources hypothesis. By investigating the causal relationship between environmental and financial performance, the authors suggest a bidirectional causality between CEP and CFP. In the short run, which is defined as one year, CFP can increase a firm’s environmental performance in accordance with the slack resources hypothesis. Nevertheless, in the long run, referring to a period of more than one year, this effect might disappear. Looking at the other direction of the relationship, it is apparent that increasing environmental performance has no short-term effect on a corporate financial performance, while a firm will significantly benefit in the long term.43Hang, M., Geyer‐Klingeberg, J., & Rathgeber, A. W. It is merely a matter of time: A meta‐analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment, 28(2), 257-273 (2019).

In the meta-analysis of Earnhart (2018), the author finds mixed evidence on the impact of environmental performance. He states that the influence varies based on the specific financial performance metric and environmental performance indicator utilized in each individual empirical investigation.55 Earnhart, D. The effect of corporate environmental performance on corporate financial performance. Annual Review of Resource Economics, 10, 425-444 (2018).

Finally, Chowdhury et al. (2023) gives an overview of the empirical literature in the field of CEP-CFP.56Chowdhury, S. B., DasGupta, R., Choudhury, B. K., & Sen, N. Evolving alliance between corporate environmental performance and financial performance: A bibliometric analysis and systematic literature review. Business and Society Review, 128(1), 95-131 (2023). The paper provides evidence that in the initial phase of 1994-2014, the question of “Does it pay to be green” was in the main focus. During the subsequent period (2015–2022), publications added to the body of knowledge from diverse angles. These encompassed the effectiveness of proactive environmental strategies, technology-driven innovations, the significance of stakeholder engagement approaches, the evolving role of corporate environmental disclosure as a means of stakeholder connection, the implementation of ESG models in the context of the CEP–CFP relationship, and the influence of corporate governance on sustainability initiatives. These contributions also included new approaches in corporate social responsibility. According to the authors, these findings make a significant contribution to the literature across different time periods, underscoring the evolutionary trajectory of the CEP–CFP domain.56Chowdhury, S. B., DasGupta, R., Choudhury, B. K., & Sen, N. Evolving alliance between corporate environmental performance and financial performance: A bibliometric analysis and systematic literature review. Business and Society Review, 128(1), 95-131 (2023).

2.3 Summary of relevant Literature

Concerning the causal effect of the CEP-CFP relationship, the following main take-aways can be derived from the analysis of recent literature:

- The sign of the relationship (negative/positive) depends on the level of CEP according to Horváthová (2010)57Horváthová, E. Does environmental performance affect financial performance? A meta-analysis. Ecological economics, 70(1), 52-59 (2010). and Trumpp & Guenther (2017)54Trumpp, C., & Guenther, T. Too little or too much? Exploring U‐shaped relationships between corporate environmental performance and corporate financial performance. Business Strategy and the Environment, 26(1), 49-68 (2017).– in accordance with the slack resources hypothesis.

- The sign of the relationship (negative/positive) depends on the time. Horváthová (2010)57Horváthová, E. Does environmental performance affect financial performance? A meta-analysis. Ecological economics, 70(1), 52-59 (2010). & Hang, Klingeberg & Rathgeber (2018)43Hang, M., Geyer‐Klingeberg, J., & Rathgeber, A. W. It is merely a matter of time: A meta‐analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment, 28(2), 257-273 (2019). found an intertemporal effect which is in line with Porters Hypothesis.

- In accordance with the instrumental stakeholder theory, a bidirectional relationship can only be partially proven.

- Various contextual factors need to be considered: industry characteristics & dynamics, regulations, and regional differences.

Broadly speaking, most of the recent literature sums up, that a generally positive linkage between CEP-CFP can be found, which means that the BCS exists. Particular attention should also be drawn to the publication rate: the annual publication shows a growth trend from 2015 onwards where almost 82% of total publications take place. This indicates increasing attention in academia amidst regulatory reforms and pressure from stakeholders in different countries.56Chowdhury, S. B., DasGupta, R., Choudhury, B. K., & Sen, N. Evolving alliance between corporate environmental performance and financial performance: A bibliometric analysis and systematic literature review. Business and Society Review, 128(1), 95-131 (2023).

Limitations & Future Research

The CEP-CFP link is the central instrument in empirical research for determining the BCS. Based on the outcomes of the different studies, it appears that several limitations need to be considered.

Firstly, the reliance on various meta-analyses introduces a significant challenge due to the diverse methods and data used across these primary analyses. Each meta-analysis draws from studies that have employed distinct approaches, including variations in methodologies, data sources, and analytical techniques. For instance, the incorporation of regional differences and industry-specific nuances further adds complexity to the analysis.

The volume of conducted meta-analyses and the process of selecting specific meta-analyses are also aspects that warrant careful consideration. The number of available meta-analyses can vary significantly, and selecting the most appropriate ones for inclusion may not always be straightforward. The reliability and credibility of these meta-analyses can vary which can influence the overall findings and conclusions of the study. These factors may impact the generalizability and robustness of the findings, emphasizing the need for cautious interpretation and underscoring the necessity for further research to address these limitations comprehensively. For example, a core problem in studies linking CSP/CEP and CFP is a social desirability and significance bias. Analyses that do not find a statistically significant effect tend to not be published in scientific journals, suggesting that such the current literature tends to be biased toward studies that either show a negative or positive relationship (rather than none). Also, given that environmental and social activities are desirable for both society and sustainability researchers, it seems probable that in several cases analyses that found negative relationships between CSP/CEP and CFP ended up not being published. This would result in studies with negative findings being underrepresented in scientific journals, leading to meta analyses being biased as well.

One way to address such biases lies in conducting more primary experimental studies and studies that exploit exogeneous shocks to reveal insights into the causal relationship between CSP/CEP and CFP. In fact, recent years have seen a rise in such studies, which has helped further improve our understanding of the CSP/CEP-CFP relationship.

3 Drivers and Barriers

In practice different factors in the market influence the commercial success of the BCS. These can act as a driver of the business case.7Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business cases for sustainability: The role of business model innovation for corporate sustainability. International Journal of Innovation and Sustainable Development 6, 95-119 (2012). Even though literature refers to these aspects primarily as drivers, they can also influence the economic success of the BCS in a negative way and thus act as a barrier of the BCS. The following sections provide an overview of the most important factors that shape the emergence of a business case for sustainability.

Employees

Employees are considered one of the most valuable resources of a company as motivated and well-trained employees can increase the performance of a company and thus its profits.58Le, L., Nie, D., Ta, A., & Prybutok, V. Employee competency, diversity, and firm value. Journal of Corporate Accounting & Finance, 34(2), 109-134 (2023). Employees increasingly value sustainability and put their focus on this topic and thus have important implications for the realization of the BCS.59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016). Specifically, sustainable practices has positive effects on the recruitment of talent, the motivation and productivity of employees as well as retaining employees in the company.

Studies show that ESG performance is connected to a positive impact on a company’s attractiveness to potential employees.60Liu, L., & Nemoto, N. Environmental, social and governance (ESG) evaluation and organizational attractiveness to prospective employees: Evidence from Japan. Journal of Accounting and Finance, 21(4), 14-29 (2021).,61Turban, D. B., & Greening, D. W. Corporate social performance and organizational attractiveness to prospective employees. Academy of management journal, 40(3), 658-672 (1997). As working for a company with responsible practices in place provides their employment with a greater meaning.62Lacy, P., Cooper, T., Hayward, R., & Neuberger, L. A new era of sustainability. UN Global Compact, Accenture. (2010). In addition to that, not only the attractiveness is positively influenced by sustainable business practices. Studies also indicate that there is a positive impact on employees that are already working for the company. Not only their motivation and productivity increases, but also employee fluctuation decreases for companies that implement sustainable practices.63Kreiss, C., Nasr, N., & Kashmanian, R. Making the business case for sustainability: how to account for intangible benefits—a case study approach. Environmental Quality Management, 26(1), 5-24 (2016)., 59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016). Reducing employee retention has an important impact on the costs companies have to pay for their workforce. The recruitment of new talents as well as costs for training new employees with the skills needed, substantially increases if employee fluctuation increases.63Kreiss, C., Nasr, N., & Kashmanian, R. Making the business case for sustainability: how to account for intangible benefits—a case study approach. Environmental Quality Management, 26(1), 5-24 (2016). Thus, companies can reduce their costs and increase their performance when implementing a BCS. It is important to note that these studies can only be applied to employees that value sustainability. Therefore, the implementation of sustainable practices in the context of the BCS might also have negative effects on potential employees and employees that are working in the company already, but this is not further analyzed in empirical literature.

Risk management

Firms are exposed to many risks in the market. Especially as climate change is progressing risks like weather extremes increase, which impact companies in various ways.64Intergovernmental Panel on Climate Change. Chapter 11: Weather and Climate Extreme Events in a Changing Climate https://www.ipcc.ch/report/ar6/wg1/chapter/chapter-11/ (2023). In contrast to the risks that regularly occur in markets, environmental risks cannot be influenced by businesses and furthermore have multilayered impacts on companies.59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016).

Thus, it is recommended to adapt to these risks in order to reduce costs that can arise when such risks materialize. The BCS provides companies with options to prepare for these risks by implementing sustainable practices. A large body of literature concluded that implementing actions aimed at increasing sustainability of a company reduces environmental risks.65Ambec, S., & Lanoie, P.. Does it pay to be green? A systematic overview. The Academy of Management Perspectives, 45-62 (2008). , 59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016). , 66Carroll, A. B., & Shabana, K. M. The business case for corporate social responsibility: A review of concepts, research and practice. International journal of management reviews, 12(1), 85-105 (2010).

In practice, companies whose value creation depends largely on land use, such as Unilever, Mars, and Nespresso, intended to reduce their risk of rendering land unusable and increase the resilience to weather extremes by investing in the Rainforest Alliance.59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016).

To conclude, the reduction of risk is a driver for the implementation of the BCS as the implementation can help to control risks and lower the impacts they have on companies. The most important reason why the reduction of risks is a driver of the BCS is that potential costs induced by those risks are substantially lowered.67Basel Committee on Banking Supervision. Climate-related risk drivers and their transmission channels https://www.bis.org/bcbs/publ/d517.pdf (2021).

Innovation

Solving environmental issues in many cases requires the innovation of products or processes.68Pinkse, J., & Bohnsack, R. Sustainable product innovation and changing consumer behavior: Sustainability affordances as triggers of adoption and usage. Business Strategy and the Environment, 30(7), 3120-3130 (2021). Furthermore, innovation helps to act on the increasing demands of consumers for sustainable products.69Economist Intelligence Unit. An Eco-wakening Measuring global awareness, engagement and action for nature. (2021).

The BCS not only addresses the increasing demand for sustainable products but further helps to solve problems that consumers are faced with, which can increase customer retention.70Schaltegger, S. & Wagner, M. Managing and Measuring the Business Case for Sustainability. Capturing the Relationship between Sustainability Performance, Business Competitiveness and Economic Performance. in Managing the business case for sustainability: the integration of social, environmental and economic performance. (eds. Schaltegger, S. & Wagner, M.) 1-27 (Greenleaf, 2006). For example Procter & Gamble reduced their consumers electricity costs by developing detergents that can be used for washing clothes at low temperatures and thus decreased the energy used for heating water.59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016).

This is also an example of the fact that the capability to innovate provides companies with new business opportunities. Furthermore, innovative products can be sold at higher prices as consumers tend to have a higher willingness to pay for innovations that cannot be provided by other products.126 In addition to product innovations, the innovation of production processes also provides opportunities to increase efficiency and lower costs. For example, the company 3M, a technology company, innovated by product reformulation, the reconditioning of production equipment and by that managed to increase the efficiency of waste management and lowered their pollution.713M. Das Unternehmen https://www.3mdeutschland.de/3M/de_DE/unternehmensinformationen/ (n.d.)., 59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016). However, it needs to be considered that innovation requires the adoption of processes, resources used, the training of employees and other aspects which incur costs.72Yeboah, A. Innovation process model: An integration of innovation costs, benefits and core competence. Cogent Business & Management, 10(1), 1-23 (2023).

Thus, innovation provides companies with an incentive to implement a BCS as this holds opportunities to lower costs and broaden the customers they are selling to. However, potential innovations may also hinder the implementation if companies perceive that the implementation and development of such innovations will incur higher costs than it will bring benefits.

Reputation

The reputation of a company is a very important resource as companies with a good reputation appeal to a wider range of customers and thus have the opportunity to charge higher prices as their products and services are perceived as worthier and tend to have lower costs of capital and a higher market value.73Eccles, R. G., Newquist, S. C. & Schatz, R. Reputation and Its Risks https://hbr.org/2007/02/reputation-and-its-risks (2007).

As consumers increasingly value sustainability and about 84% consider sustainability aspects when making purchase decisions they search for companies that provide them with such a standing.74Rogers, K., Costgrove, A. The CEO Imperative: Make sustainability accessible to the consumer. https://www.ey.com/en_gl/consumer-products-retail/make-sustainability-accessible-to-the-consumer#:~:text=84%25%20say%20sustainability%20is%20important,from%20the%20risk%20of%20infection (2021). It is observed that the implementation of sustainable practices has a positive impact on the reputation of a company and thus its value.75Kurucz, E. C., Colbert, B. A., & Wheeler, D. (2008). The business case for corporate social responsibility. in The Oxford handbook of corporate social responsibility. (eds. Crane, A., McWilliams, A., Matten, D., Moon, J., & Siegel, D. S.) 83-112 (OUP Oxford, 2008)., 76Peters, J., & Simaens, A. Integrating sustainability into corporate strategy: A case study of the textile and clothing industry. Sustainability, 12(15), 6125, 1-35 (2020). One example where a company could have potentially lowered their costs by implementing sustainable practices in the first place is when NGOs accused Nike of supporting child labor along their supply chain and consequently their sales dropped.70Schaltegger, S. & Wagner, M. Managing and Measuring the Business Case for Sustainability. Capturing the Relationship between Sustainability Performance, Business Competitiveness and Economic Performance. in Managing the business case for sustainability: the integration of social, environmental and economic performance. (eds. Schaltegger, S. & Wagner, M.) 1-27 (Greenleaf, 2006).

In conclusion the changes in reputation encourage companies to implement a BCS as it provides them with a wider range of customers as well as possible business partners and therefore provides business opportunities.76Peters, J., & Simaens, A. Integrating sustainability into corporate strategy: A case study of the textile and clothing industry. Sustainability, 12(15), 6125, 1-35 (2020).

Regulations

Without regulations like taxes or pollution permits, which confront companies with the costs incurred through their value creation, businesses create too much pollution and use resources in an unsustainable manner in many cases. If those practices are perceived as being more profitable, there would be no incentive to reduce those negative aspects.65Ambec, S., & Lanoie, P.. Does it pay to be green? A systematic overview. The Academy of Management Perspectives, 45-62 (2008). Furthermore, in many situations firms are not aware of the benefits the implementation of BCS holds for them.66Carroll, A. B., & Shabana, K. M. The business case for corporate social responsibility: A review of concepts, research and practice. International journal of management reviews, 12(1), 85-105 (2010). Many managers perceive that implementing environmentally friendly practices incurs costs. In those cases, regulations provide opportunities to make sustainable practices more profitable compared to conventional business practices.77Revell, A., & Blackburn, R. The business case for sustainability? An examination of small firms in the UK’s construction and restaurant sectors. Business strategy and the environment, 16(6), 404-420 (2007). In contrast to this, regulations are sometimes perceived to be connected to costs, as firms would have reduced their impact on the environment if it would have been profitable.78Dechezleprêtre, A., Koźluk, T., Kruse, T., Nachtigall, D., & De Serres, A. Do environmental and economic performance go together? A review of micro-level empirical evidence from the past decade or so. International Review of Environmental and Resource Economics, 13(1-2), 1-118 (2019). For this reason, it is argued that environmental regulations reduce the competitiveness of firms. However, with the focus on the BCS regulations can be seen as a driver, as they incur costs for not implementing sustainable practices thus making the implementation of sustainability more profitable than doing business the conventional way. However, it can be argued that it is not only a driver but rather makes the implementation of sustainability mandatory.

Costs

The reduction or increase of costs is one of the most important factors that influences the implementation of BCS. Thus, it is analyzed in the majority of literature and as mentioned in section 2.1 hypothesis like the win-win hypothesis and the Porter hypothesis have been developed to account for these implications.

Many studies indicate that the costs of implementing a BCS, for example through implementing new technologies, or training employees for new processes, are perceived to be higher than the actual benefits the BCS can provide.77Revell, A., & Blackburn, R. The business case for sustainability? An examination of small firms in the UK’s construction and restaurant sectors. Business strategy and the environment, 16(6), 404-420 (2007)., 79Revell, A., Stokes, D., & Chen, H. Small businesses and the environment: turning over a new leaf?. Business strategy and the environment, 19(5), 273-288 (2010). In practice companies might also hesitate to implement sustainable products as the materials for such products are more expensive than the prices of conventional materials.80Gammage, E. Are sustainable products more expensive? https://www.savemoneycutcarbon.com/learn-save/are-sustainable-products-expensive/ (n.d.) In line with the perception that the implementation of BCS is connected to higher costs is the finding of Revell et al. (2007) that a majority of small and medium sized enterprises consider increased costs as a barrier for improving sustainability.77Revell, A., & Blackburn, R. The business case for sustainability? An examination of small firms in the UK’s construction and restaurant sectors. Business strategy and the environment, 16(6), 404-420 (2007).

In contrast to these findings the implementation of sustainable business practices holds diverse opportunities for reducing costs. These cost reductions are encouraging companies to implement BCS. Some opportunities to reduce costs have already been analyzed in the sections before, for example the decrease in employee retention, managing risks through sustainable practices and innovating products or processes. In addition to that optimizing production processes also holds the potential to increase the efficiency of resource use and thus reduce the costs, the company has to bear for such resources.59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016).

In conclusion costs can hinder the implementation of BCS if the costs of implementation are perceived to exceed its benefits. However, they are more likely to be considered a driver as the implementation provides various opportunities to decrease costs and thus have a positive impact on the value generation of the company.

Financial performance

The final driver or barrier to the BCS is the financial performance of companies. As stated in chapter 2 the connection between CEP, CSP and CFP has been analyzed for a few decades now and concluded that the implementation of sustainable business practices is generally considered to have a positive impact on the financial performance of companies and thus can be seen as a driver for the BCS. Furthermore, chapter 2 finds that financial performance is impacted by corporate environmental performance. Moreover, companies engaging in sustainable practices have experienced higher sales growth and lower cost of debt. Additionally, during crisis the share prices of companies that have responsible business practices in place are more stable than for companies that have not implemented such practices.59Whelan, T., & Fink, C. The comprehensive business case for sustainability. Harvard Business Review, 21(2016) (2016). In the above sections different aspects have been analyzed and positive as well as negative relations could be observed in connection with environmental practices and financial performance.

As BCS are only implemented if there is a positive impact on potential profits, financial performance can act as barrier if the financial performance would be negatively affected by the sustainable business practices. Overall, the analysis implies that financial performance can be seen as a driver as well as a barrier of the BCS.

4 Practical Implementation

In practice, it seems difficult for companies to apply and implement the identified theoretical contents to their specific businesses. Therefore, the implementation part suggests steps that could support companies in implementing the BCS, as well as tools and two examples that have already successfully completed the steps. If a company management wants to implement the BCS, it is less about the basic plan of a business venture – compared to the original Business Case when starting the company or developing a new product range – and more about adapting it to be more sustainable.

However, due to the fact that companies are founded and managed for economic purposes, it is necessary for their management to develop the majority of its social commitment in the context of the company’s economic goals.81Kramer, M. R. & Porter, M. Creating shared value. Harvard Business Review 17 (2011).82Parnell, J. A. Sustainable strategic management: construct, parameters, research directions. International Journal of Sustainable Strategic Management 1, 35-45 (2008). The management must recognize, establish and strengthen the links between non-monetary social and environmental activities on the one hand and business or economic success on the other.81Kramer, M. R. & Porter, M. Creating shared value. Harvard Business Review 17 (2011).,83Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business Cases for Sustainability and the Role of Business Model Innovation: Developing a Conceptual Framework. SSRN Journal (2011) As mentioned in the definition part above, the goal and purpose of the BCS is to create this link so that economic success is created from environmental and social activities.83Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business Cases for Sustainability and the Role of Business Model Innovation: Developing a Conceptual Framework. SSRN Journal (2011) Research by Schaltegger & Wagner (2006) indicates that most companies have the potential for one or even several BCS’s, but this must be actively created through intelligent sustainability management.70Schaltegger, S. & Wagner, M. Managing and Measuring the Business Case for Sustainability. Capturing the Relationship between Sustainability Performance, Business Competitiveness and Economic Performance. in Managing the business case for sustainability: the integration of social, environmental and economic performance. (eds. Schaltegger, S. & Wagner, M.) 1-27 (Greenleaf, 2006).

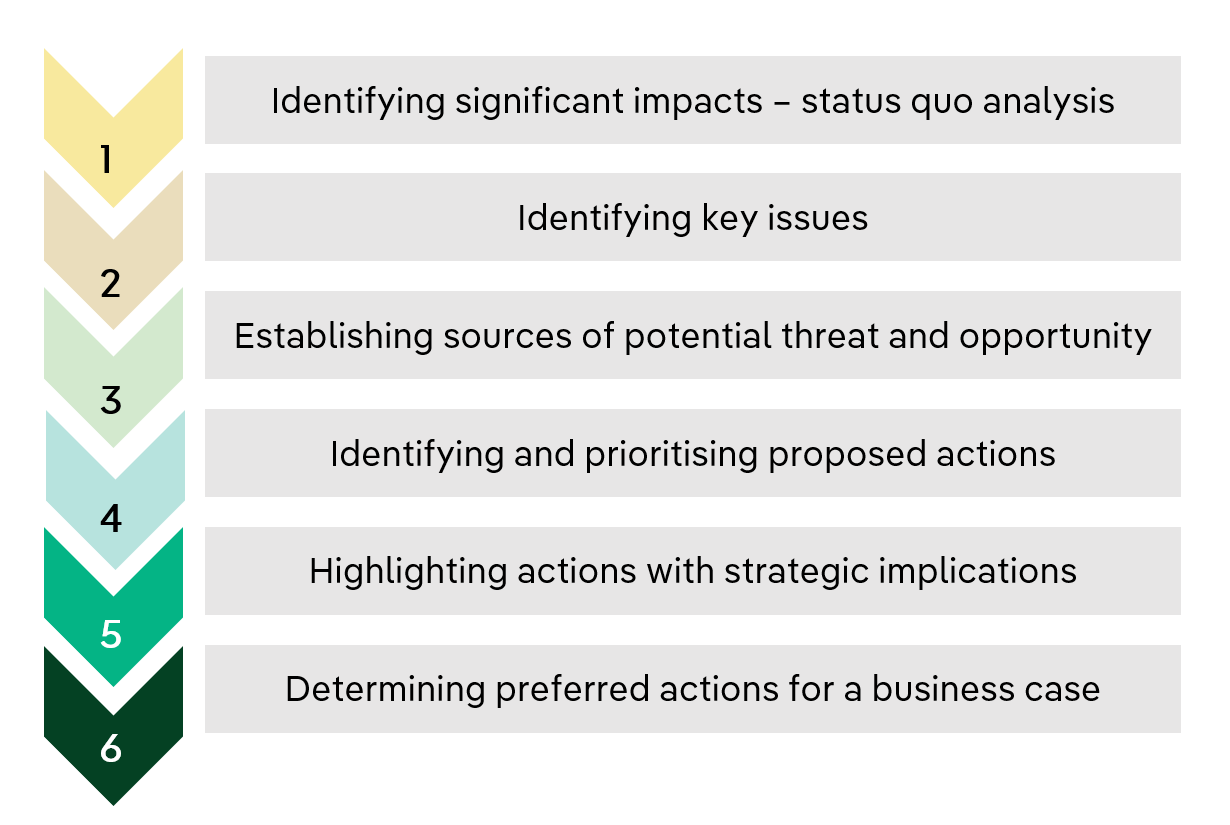

Kemp in cooperation with the World Wide Fund for Nature (WWF) (2002) presents a roadmap concept, which supports the development of the BCS in a company through six steps.

Step 1: Identifying significant impacts

The first phase (Step 1) involves a status quo analysis and is denoted as “identification of significant impacts”. This stage aims to comprehend the environmental consequences resulting from the company’s current business model and its manufactured products. The most efficient approach to pinpointing specific environmental and social effects is to carry out a thorough examination or evaluation of the company. For example, one outcome could be the determination of the total greenhouse gas emissions. There are various tools that could be used for this step, most of which are based on scientific principles, such as the Environmental Impact Assessment.84Kemp, V. & Loop Environmental Networks Ltd. To whose profit? Building a business case for sustainability. WWF-UK (2002).

Step 2: Identifying key issues

In the next step (Step 2), an assessment is made to ascertain whether the identified impacts possess immediate or future external significance, the “identification of key issues”. This is also the step to identify operational units where opportunities could arise to create value through improved ethical, environmental, and social performances. As a company, it is important to know the stakeholders for sustainability issues as well as the main drivers for change (here not explicitly the BCS). These are, according to Kemp, globalisation, global wealth or poverty distribution, government and laws, environmental concerns, social expectations, and lastly pressure from employees, investors, and consumers.84Kemp, V. & Loop Environmental Networks Ltd. To whose profit? Building a business case for sustainability. WWF-UK (2002). This largely coincides with the identified main stakeholder groups by Kreiss et al. (2016): Community, Customer, Employees, Government, and Investors.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016). For the BCS, the focus on society is particularly important and thus put at the centre of the strategy.86Yadav, N. & Mankavil Kovil Veettil, N. Developing a comprehensive business case for sustainability: an inductive study. International Journal of Organizational Analysis 30, 1335–1358 (2022). For this, tools such as an issue or stakeholder matrix or the stakeholder dialogue can be used.

Step 3: Establishing sources of potential threat and opoprtunity

The third step (Step 3) involves analysing the recognized problems to ascertain whether they could offer a chance or pose a danger to the company. Proprietary risk assessment instruments and similar resources can aid managers in comprehending the character and scope of these threats.84Kemp, V. & Loop Environmental Networks Ltd. To whose profit? Building a business case for sustainability. WWF-UK (2002). For a well-defined BC, managers must identify the drivers that steer social and environmental achievements and how these accomplishments impact the company’s ultimate, enduring profitability. This amplified emphasis on exhaustive identification and measurement of performance drivers is also mirrored in prevailing management ideologies.87Epstein, M. J. & Roy, M.-J. Making the business case for sustainability: Linking social and environmental actions to financial performance. Journal of Corporate Citizenship 9, 79–96 (2003)., 83Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business Cases for Sustainability and the Role of Business Model Innovation: Developing a Conceptual Framework. SSRN Journal (2011) Schaltegger et al. (2011) further investigate the interactions between drivers and sustainability strategy on the one hand, and business model innovation on the other hand as mentioned in chapter 1.4.83Schaltegger, S., Lüdeke-Freund, F. & Hansen, E. G. Business Cases for Sustainability and the Role of Business Model Innovation: Developing a Conceptual Framework. SSRN Journal (2011) An in-depth analysis of the drivers and barriers of the BCS was already covered in Chapter 3.

Step 4: Identifying and prioritising proposed actions

The next step (Step 4) is to decide whether the topics either offer opportunities for competitive advantage or are of strategic importance for the company. It must be analysed whether they are compatible with the corporate strategy or whether they can be integrated into the business strategy in such a way that additional value is created. This corresponds to the basic concept of creation of shared value, mentioned in chapter 1.4. To assess the relevance for the company they should be measurable in terms of costs and benefits.84Kemp, V. & Loop Environmental Networks Ltd. To whose profit? Building a business case for sustainability. WWF-UK (2002).

A distinction can be made between actions whose benefits are directly measurable, based on “hard” facts, and those that are much more difficult to measure.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016). Tangible benefits derived from sustainability initiatives are characterised, for example, by cost reduction or increasing efficiency. They can be directly expressed in numbers to assess whether an investment is worthwhile, for example savings in energy, waste and emissions. However, for the creation of a robust BCS, it requires the inclusion of intangible benefits, encompassing all levels of value creation.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016)., 88Presley, A. & Meade, L. M. The Business Case for Sustainability: An Application to Slow Fashion Supply Chains. IEEE Engineering Management Review 46, 138–150 (2018). Intangible benefits arise, for example, from positive effects resulting from the increased sustainability of the company, such as stronger employee loyalty, a better image with customers or a better position with investors. In practical application, it is often difficult to measure only the effects of sustainability measures. This applies to both benefits, tangibles and intangibles.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016)., 86Yadav, N. & Mankavil Kovil Veettil, N. Developing a comprehensive business case for sustainability: an inductive study. International Journal of Organizational Analysis 30, 1335–1358 (2022).

Demonstrating sustainability-specific effects in this context has proven to be challenging due to their interconnection with other financial information within the company, rendering their quantification either excessively complex or unnecessary.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016). When it comes to intangible benefits, many can be evaluated qualitatively, obviating the need for quantification. Businesses that are attentive to their stakeholders’ demands can assign greater significance to qualified intangible benefits in business scenarios. Employing a return on investment (ROI) methodology, utilizing measurable indicators associated with the particular intangible benefit being portrayed, is one approach for quantifying intangible advantages.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016)., 89Phillips, J., Phillips, P. & Pulliam, A. The ROI methodology: a tool to measure and improve. Measuring ROI in Environment, Health, and Safety. (Wiley Online Books 2014). In practice, employee satisfaction and retention, measured by reduced absenteeism and health care costs, have proven useful for quantification.85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016). Two other tools that may be mentioned are the “total cost assessment methodology” and the “SDEffect”. The former is primarily intended to enable the inclusion of all costs or their avoidance in the estimation of sustainable projects, while the latter is a framework developed exclusively for sustainability projects that can be used to measure how sustainability initiatives affect the market value of a company. This is done along the lines of traditional accounting tools “ratio analysis”, “discounted cash flow analysis”, “rule of thumb valuations”, “economic value-added analysis”, and “option pricing”.90American Institute of Chemical Engineers’ Center for Waste Reduction Technologies. Total cost assessment methodology – internal managerial management decision making tool. (1999)., 85Kreiss, C., Nasr, N. & Kashmanian, R. Making the Business Case for Sustainability: How to Account for Intangible Benefits – A Case Study Approach. Environmental Quality Management 26, 5–24 (2016)., 86Yadav, N. & Mankavil Kovil Veettil, N. Developing a comprehensive business case for sustainability: an inductive study. International Journal of Organizational Analysis 30, 1335–1358 (2022).

The results of these assessments can be documented in the form of a concise selection of prioritized actions. These actions are determined based on factors such as their ability to generate and sustain value, alignment with the overarching corporate strategy, and practical feasibility. This information serves as the foundation for a business case that centers on opportunities for value creation and sustainability. The analysis may also indicate the necessity for a fundamental re-evaluation of existing strategic intentions. Management can support itself in this phase by employing a combination of techniques. Firstly, tools are required to check the company’s business operations for external influences. Many of these tools rely on key market dynamics to identify potential sources of competitive advantage. In addition, tools and measures help to assess whether the actions derived eventually bring potential benefits to the company. It is recommended to use the most important financial drivers and indicators. Cost-benefit methods can be used at this point and usually include both quantitative and qualitative information in the analysis process.84Kemp, V. & Loop Environmental Networks Ltd. To whose profit? Building a business case for sustainability. WWF-UK (2002).

Step 5: Highlight actions with strategic implications